Natural elements – whether as real materials or design inspiration – remained a top trend…

Read More →

Natural elements – whether as real materials or design inspiration – remained a top trend…

Read More →

The chief creative director for the award-winning British brand talks about how Pooky’s colorful, whimsical…

Read More →

One popular trend in lighting design is a pared-down aesthetic that can look organic or…

Read More →HIRI’s executive director distills what the organization is hearing from consumers about their home improvement spending plans.

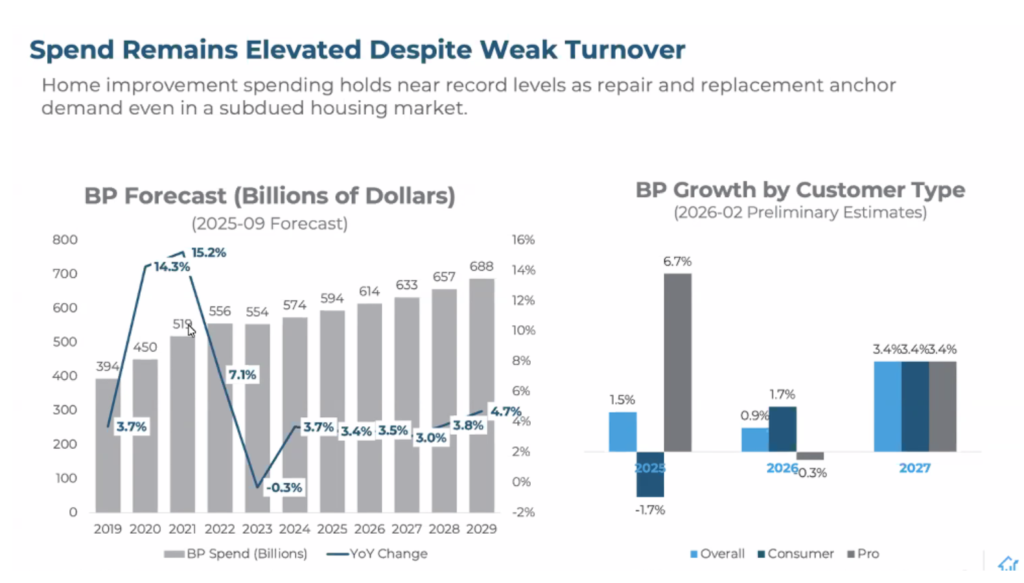

In a lot of ways, “2026 is going to feel a lot like 2025,” noted Dave King, executive director of the Home Improvement Research Institute (HIRI), during a recent webinar. He mentioned that HIRI looked back over its 2025 data and has revised its forecast from Q3 2025. “We revised down from 3.7% to 1.5% — and that’s a meaningful shift down since September,” he said. “It’s been a tumultuous time, with the government shutdown and all that it entailed. There’s a lot of conversation about tariffs right now, especially with the Supreme Court coming out with its stance. We’re trying to figure out how these things will land. It’s also obvious there’s going to be some debate about rebates and what the president can and can’t do as it relates to tariffs.”

All that said, King noted that 1.5% growth is still a positive. He stated, “This is temperate growth. It’s not negative – and that’s great – but how much of that is inflation, how much of it is actual growth, and how does this impact different building product categories?”

At the time of the webinar, the International Builders’ Show had just concluded in Las Vegas and King mentioned that he listened to what companies at the show were saying about the year ahead and how their businesses are faring.

“The consensus is a hyper-focus on gaining market share,” he said. “This is not a ‘rising tide lifts all boats’ situation. From a product perspective, you have to out-compete — and this was definitely a theme in 2025. Those who grew their businesses did so by gaining market share. There were some categories that did see some growth as a vertical, but collectively, those of you who grew in 2025 should probably pat yourselves on the back for a job well done. This year is going to be even more competitive.”

What was key in 2025 were the large discretionary projects that were postponed, delayed, downsized, or cancelled. It varied by income group as to how the market adjusted to these changes, King explained.

Pressure on growth

When it comes to 2026, HIRI’s research indicates that most categories of building products will see growth only through inflation. “This matters,” King said. “We all have to figure out how to compete and have growth when costs keep going up. We’ve seen a number of ways that organizations are handling this. Some are – in the name of AI – letting staff go to keep the margins where they need to be.”

Noting pressure from Wall Street for companies to become more lean, King believes that in order to reach that goal, companies will be looking for cost-cutting measures. That pressure is expected to ramp up in 2026.

King also pointed to the National Association of Realtors (NAR) survey posed to prospective homeowners that asks whether it’s a good or bad time to buy a home. “Collectively, 73% said it’s a bad time,” he said. “That number is really high, and I think we all know why. Home prices have gone up, and we have historic levels of equity right now in homes. So, for those who are already in a home, it’s great. For everyone else, it’s a challenging time because interest rates are high. Our view of interest rates is that while there might be a mild decline over the year, there is not going to be a big shift in interest rates.”

Obviously, inflation has been a top topic among business owners everywhere. “In speaking with HIRI members, it’s our understand that 90% of the tariffs have been passed on, but with everything going on right now with the Supreme Court decision, there might be some disruption here. Our understanding is that even if the tariffs have to be largely reversed and not implemented in the future, it’s still not going to give growth and we will still see a lot of inflationary pressure.”

What homeowners are doing

Like other pundits in the home improvement and housing sector, King does not expect interest rates to drop significantly in 2026 or even in 2027. “What we are predicting is a very mild drop in rates over time,” he explained. “So anyone who is waiting until things suddenly drop, we’re just not anticipating that happening anytime over the next five years. A ‘black swan’ event could change that overnight — and if that happens, we’ll update our forecast.”

When it comes to analyzing the habits of home buyers, this year is one of toughest ones to predict. “Since 2000, we have had the fewest number of home buyers entering the market — and the next closest is 2022. We are truly in an anomaly period of time and it has real ramifications to the industry,” King said.

“A lot of the research out there compares new construction with existing, but [HIRI] has sort of flipped that idea on its head and said let’s look at the person. We know there are certain verticals – outdoor power equipment is a great example – regarding first-time home buyers. First they buy the home, and then they have to buy all of the equipment for it. This has a very disparate impact, depending on the category that you’re in,” King stated. “You might say that your particular vertical is doing better or worse than the overall average, but one of the most important questions to ask is, ‘How reliant is it on new home owners or first-time home buyers entering the market? With fewer homes being bought and sold, that negatively impacts total spend.”

The age-old model of new homes being purchased and existing homes being sold has started to struggle over the past couple of years because of an overreliance on that continual turnover, according to King. “Because we know that new home buyers and sellers spend more on their home — they’re getting ready to sell or are making their new home their own,” he said. “However, what many of these models struggle to capture was the golden interest rates of people who have mortgages under 2%, 3% and 4%. For these people, to sell their home and buy another one has become cost-prohibitive,” he added, noting that the interest rate on a new 30-year mortgage might be double the cost of their payment currently.

“As such, we are seeing more remodeling in place. That’s a major theme that we’ve seen,” King said. As he explained, if homeowners take out a home equity loan at 8% to remodel their homes the way they’d like, it’s still cheaper than selling and buying a home at current rates. “Those people are going to struggle to move in this environment,” he cautioned. As a result, any housing movement will most likely come from those who are forced to move due to their job or to be closer to family.

Renewed emphasis on remodeling

According to research, roughly 10% of the population needs to move every 10 years.

If interest rates are still above 5%, then half of that population who would normally want to move will not be doing so because of the current environment.

“Think about how that accumulates over time,” King said. “Let’s say in 2022, you’re thinking about moving. In 2023 you want to move, but you’re not going to because of the interest rates. Now it’s 2024 and your neighbor is also wanting to move, but they’re also not moving for the same reason. This creates pressure and pent-up demand for moving. If interest rates change drastically, I think we’d see an explosion of homes coming on the market. We think that if rates do decrease, they will do so mildly and very conservatively, which would make a lot more sense for the stability of our economy.”

The pandemic effect lingers — in a good way

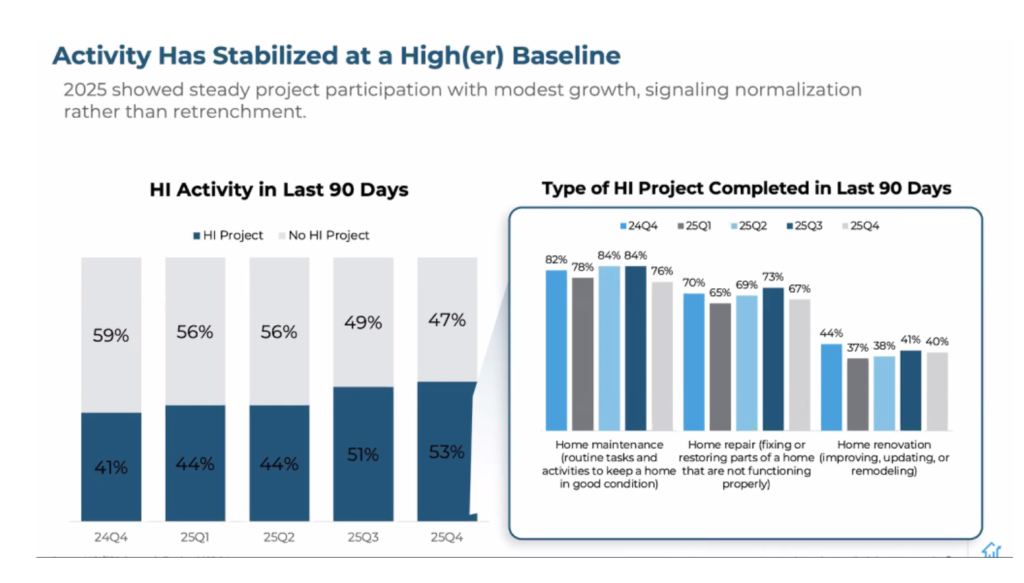

HIRI typically collects its data from two separate groups – homeowners and contractors – close to the end of each quarter. For 2025, HIRI saw a mild increase in the amount of home improvement activity, plus it observed consistency as to the type of activity.

“As the pandemic came toward the end, there was a lot of conversation as to whether home improvement was just going to drop off a cliff because no one traveled for two years and now they wanted to travel. Collectively, we didn’t see that happen,” King reported. “The pandemic led to a structural increase in the demand. It wasn’t a case of people saying, ‘I was going to wait until next year to do this project, but I’ll just do it now.’ Instead it was, ‘The pandemic helped me understand the importance and the role of the home in my personal wellbeing and happiness.’ As such, we’ve seen continued growth in the home improvement industry. The last couple of years have largely been driven by inflation, but we haven’t seen any wholesale drop that says it’s just not important to homeowners.”

Where are they spending?

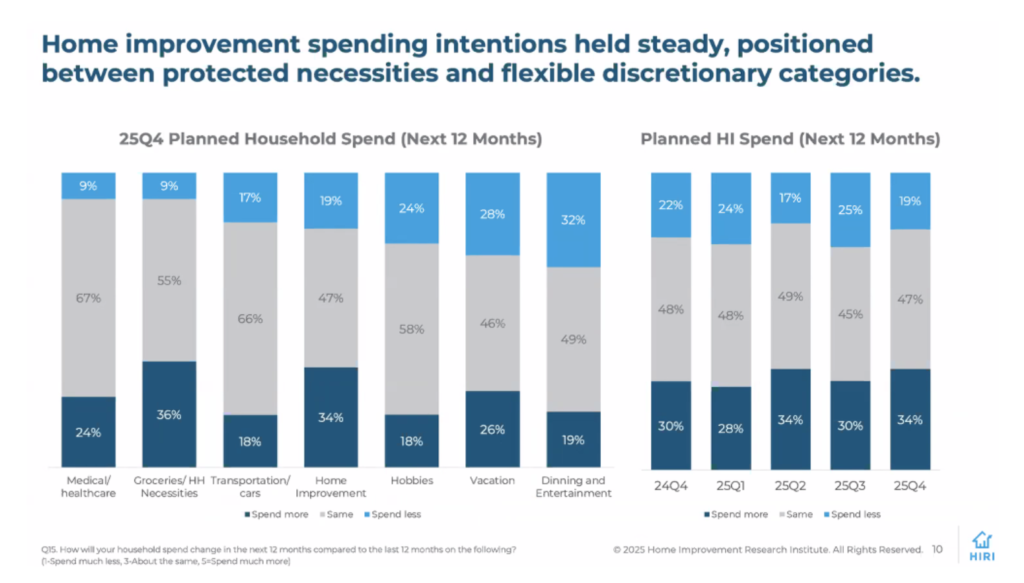

Among homeowners surveyed, 34% indicated they are looking to spend more in home improvement. “The only category that is higher than home improvement is groceries/household necessities — which is an inflationary expectation,” King explained, pointing out that the home improvement category has ranked number two in spending intentions for the past two years.

Referring to the recent Consumer Sentiment tracker numbers, released by the University of Michigan, King said HIRI does not see a correlation between consumer sentiment and building product spend. “So how we feel versus how money is spent aren’t related,” he quipped. “A better predictor than consumer sentiment is what’s happening with disposable income — and that has a four or five quarter lag. One perspective to have in mind when we forecast out disposable income is that if, fundamentally, you’re making more than you did one year ago or five quarters ago, you’re still likely to spend on home improvements.”

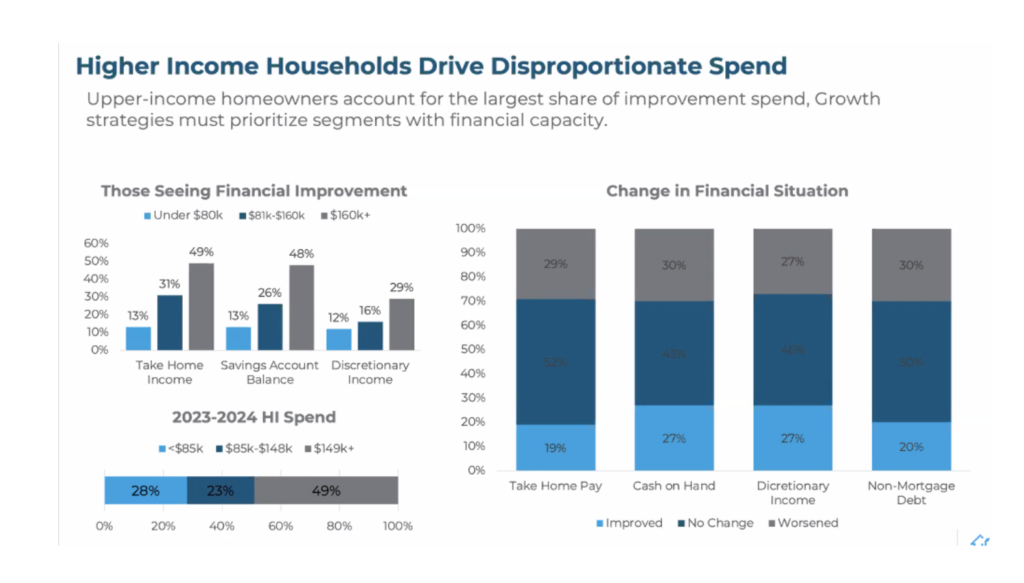

King also cited the recent National Housing Survey, provided by the Census Bureau, which polled 250,000 people. “Very consistently, the top 20% of all income earners make up 50% of home improvement spend,” he said. “Think about your business. Does it skew anything different from the national demographics? If so, it might have a disparate impact on your organization and the growth that you’re seeing or not seeing. Half of all spend is not coming from those who are under extreme pressure financially; that half is coming from those who have healthy incomes.”

Who’s doing the spending?

King noted that income levels handle their remodeling efforts differently. The upper income levels are still hiring professionals and moving forward with their projects. “There’s just a very small decrease in the percentage of work that they’re doing. Instead of going ultra-premium, they might go to premium and drop down one level.”

The middle group is the population that’s doing more DIY projects relative to what they’d want to be doing, King explained. “In other words, they still want to do the project, but they need to figure out a way to do it. So while the percentages might be a little down, those projects are still getting done via DIY. It’s the lower-income groups who are more likely to defer or delay, cancel or postpone — where a home improvement project is just not in the cards for them this year.”

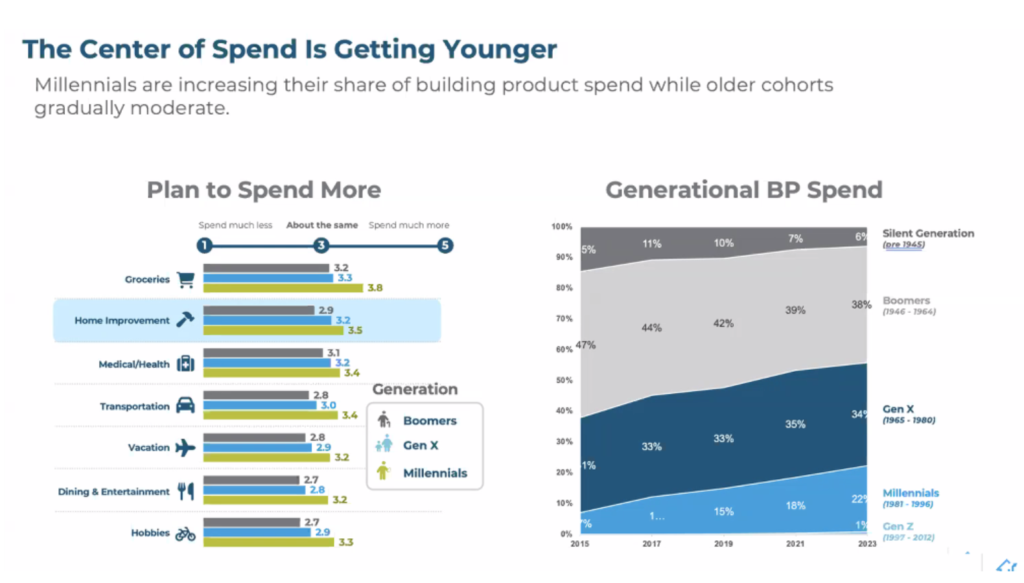

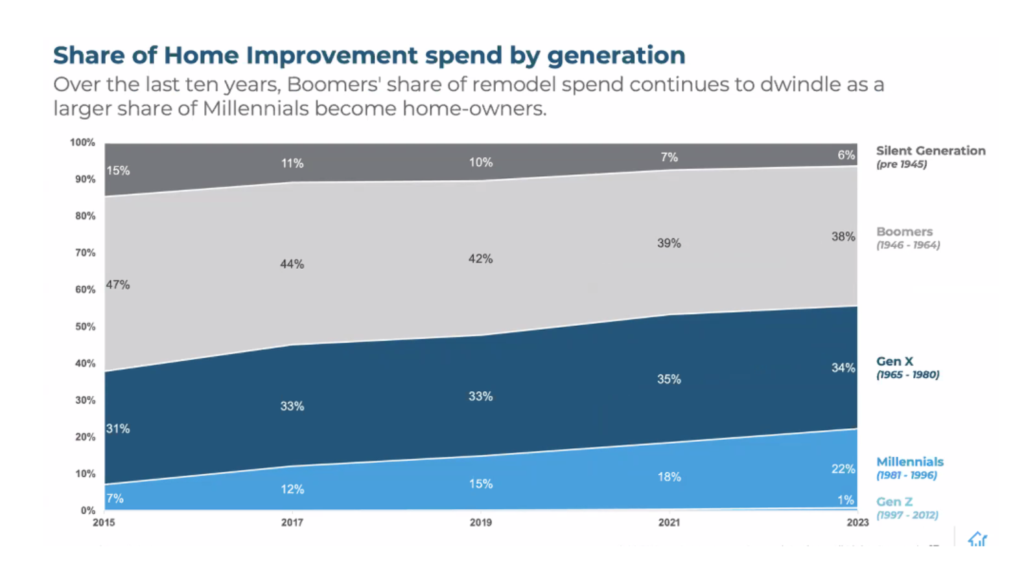

Younger generations are now showing up

The center mass of spend in building products has officially entered Gen X category, according to King. “We’re looking at that same American Housing Center data over time, and what we can see in this most recent analysis is that Gen X has hit that 50th percentile. What is important to note is the growth we’re seeing among Millennials, plus Gen Z is finally popping up on the board.”

The Millennial mindset has also shifted as they’ve gotten older. “The generation that just one decade ago was saying they don’t want to own homes, they want to share, and they want experiences are – it turns out – just getting a late start reaching these critical milestones in life. They want the same things as the generations before them, and this is very predictable [historically],” King commented. “It will continue to grow. The wave is coming. The shift between the old and the young is very predictable — we know what’s going to happen over the next 10 years.”

When HIRI researchers spoke with professionals in the remodeling industry, they found that 60% anticipate growing their business over the next 12 months. “That’s very interesting, particularly in a year where we’re flat,” King said. “There are two interesting insights to be gleaned. The first is that, generally speaking, businesses are being told that they should grow and there is a lot of pressure to grow. If the industry is flat, then part of that growth has to be at the expense of someone else — so we think that wrapped up in part of these (estimated) percentages is the mandate to grow.”

King’s advice to those businesses who count contractors as a significant portion of their sales is to know that they are hungry to grow their businesses. “Anything you can do to help them with that is going to have dividends,” he stated. “Our research shows that anything you can do to save them time – especially since there is a labor shortage – is something they’ll be willing to invest in.” The number one pain point among contractors is quality, according to HIRI research. “They don’t want to come back and have to rip something out and put something else in, because that takes up time,” he said.

Implications for 2026

King’s advice to industry professionals is to “design for the stay-driven homeowner versus the move-driven one. We still have a large part of the population who are going to be staying in place, but they still are wanting to make improvements. Make sure you are thinking of a strategy to get their attention.”

According to HIRI research, large discretionary spending in home improvement is the most challenging. Kitchen and bath cabinets were named as examples, especially since there is a lot of competition.

“If the project is a big ticket but is an emergency, they’ll spend. If it’s a small ticket discretionary spend, it’s happening,” King noted. Between those two groups lies the biggest challenge. “Meet consumers where they are, not where they aspire to be,” he advised.